Q4 2025 EdTech Market Report

.jpg)

By the end of 2025, the U.S. education technology market had fully embraced a post-boom discipline.

I. EdTech Capital Concentrates in Proven Models

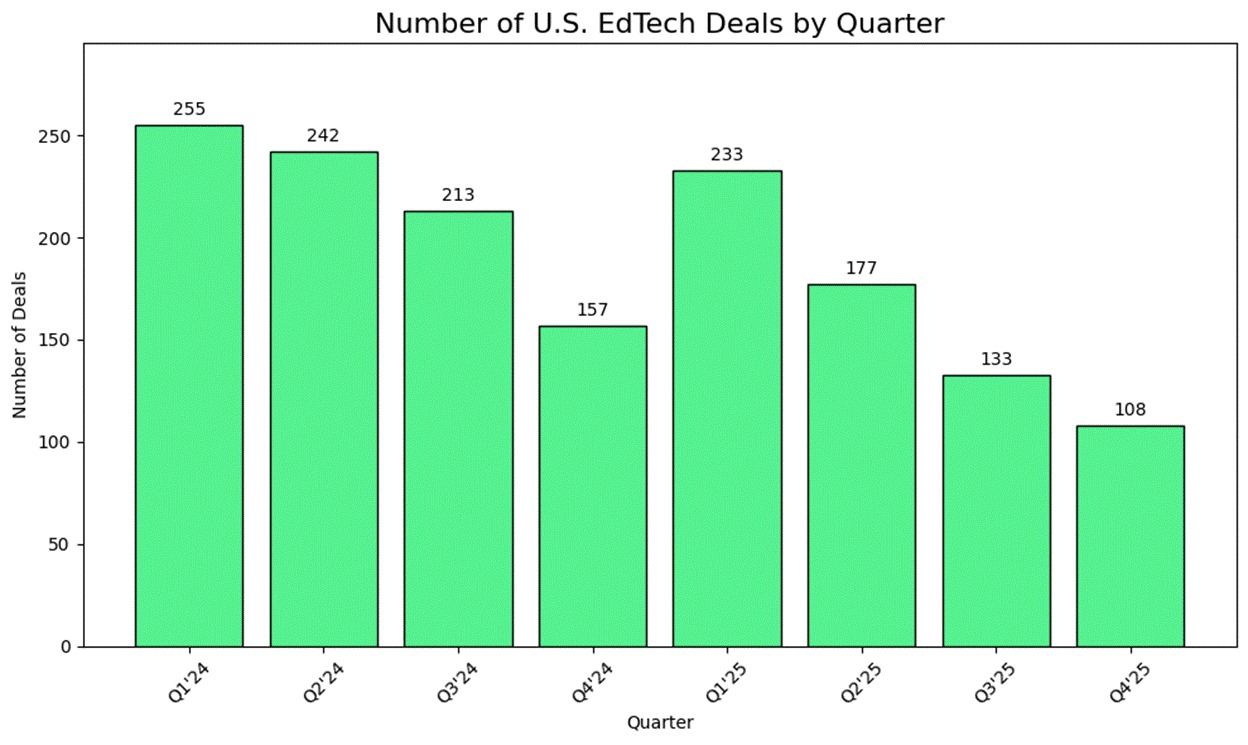

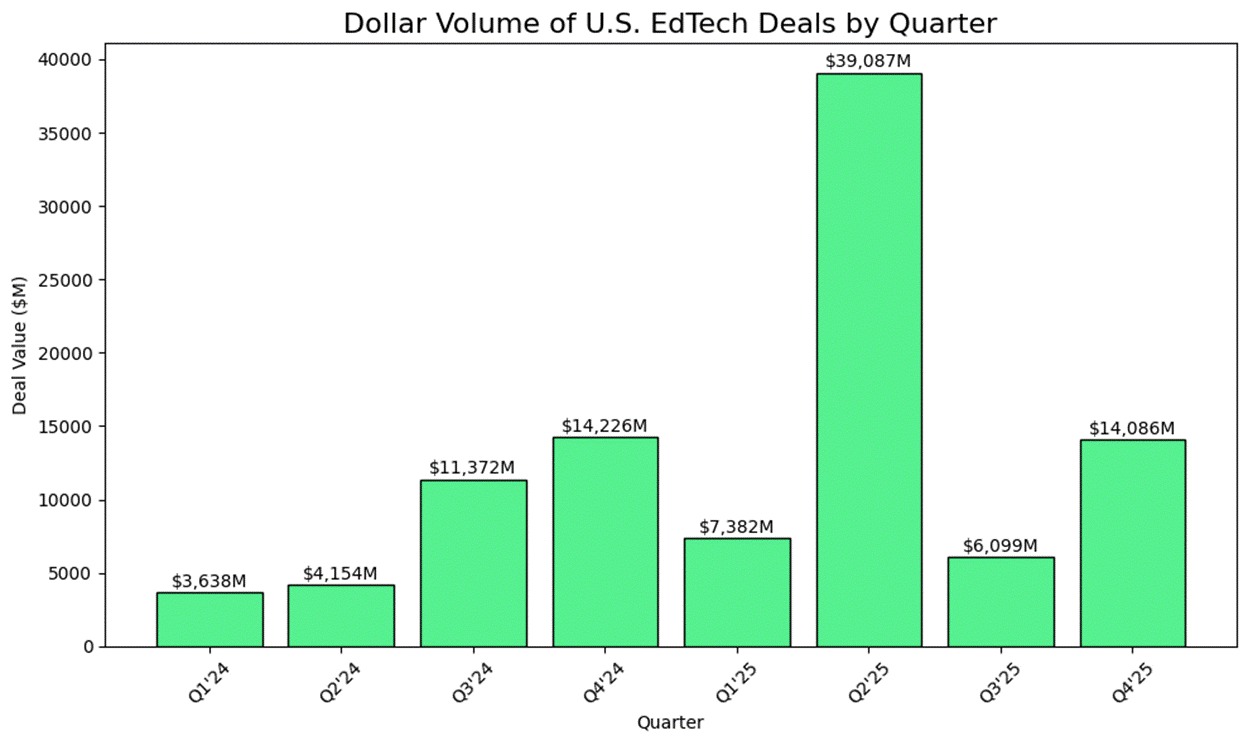

By the end of 2025, the U.S. education technology market had fully embraced a post-boom discipline. The speculative frenzy of the pandemic era was long gone, replaced by a focus on fundamentals – measurable impact, prudent capital use, and tech infrastructure that keeps schools and training programs running. In Q4 2025, roughly 240 U.S. EdTech transactions closed, a slight dip from Q3’s peak but still a robust level of activity.iv Total disclosed value topped $1 billion, achieved not via any one mega-deal but through numerous minority growth investments and structured rounds. iv

More than three-quarters of Q4 deals were non-control investments, reflecting investors’ preference to back proven winners rather than gamble on risky new entrants.iv In other words, investors are funding disciplined expansion – deeper product integrations, scalable go-to-market plans, and workflow extensions that efficiently boost customer value without over-stretching budgets. Q4 also marked the first full budgeting cycle after the K–12 stimulus (ESSER) wind-down and the FAFSA chaos in higher ed: school districts finalized their ESSER closeouts and set FY26 tech priorities, colleges operated on normalized admissions and financial-aid timelines, and government agencies continued directing funds into apprenticeships and workforce innovation. The net result is a measured, infrastructure-oriented market. EdTech remains investable, but the bar is higher, proof of impact has decisively replaced potential for scale as the key narrative for both buyers and investors.

Notably, the source of capital in Q4 was as telling as the count.

Minority private equity checks and structured growth rounds made up the bulk of funding, a classic form of “expansion capital” where investors buy into clear retention and upsell metrics rather than unproven product ideas. iv

In short, momentum investing has fully given way to precision. Capital is still available and competitive, but it’s flowing primarily to platforms that look and behave like core infrastructure in education.

II. Macro Trends: Scarcity as Strategy

Fiscal tightening continued to shape the education market’s context. The federal budget environment in late 2025 reinforced discipline: for example, the House’s FY26 appropriations draft proposed significant education cuts (a double-digit percentage cut to the Department of Education, including a 27% reduction in Title I funding), with Pell Grants flat and Work-Study funds down sharply.xiii This signaled intense scrutiny of any programs without clearly demonstrable ROI. Importantly, however, austerity was selective, not across-the-board. Funding for high-impact areas like special education, public charter schools, and career-technical programs was preserved or even increased. The policy signal was clear: fiscal restraint will continue, but evidence-backed initiatives remain protected.

Regulators also sent new signals. The Department of Education moved to tighten rules on student aid and outcomes tracking – for instance, institutions must soon report admissions data disaggregated by race and gender, a compliance shift that will ripple into enrollment management software and analytics.xi All signs point in one direction: scarcity is now a strategy. With every public dollar tied closely to outcomes, education buyers in K–12, higher ed, and workforce training are favoring platforms that offer tangible results, such as:

● Compliance assurance – tools that help meet reporting and regulatory requirements

● Operational transparency – systems that give clear visibility into usage and performance

● Measurable outcomes – solutions that can directly show improvements in student or employee success

In today’s market, vendors win only if they can prove their value, not just pitch it.

III. K–12: Building After the Boom

In the K–12 segment, the post-stimulus reality is fully in view. With federal ESSER III relief funds now expired and only narrow extensions in place, district procurement has shifted from pandemic-era experimentation to system-building. School leaders are consolidating fragmented point solutions in favor of fewer, better-integrated platforms that handle student data, attendance, staffing, and budgeting in one place.

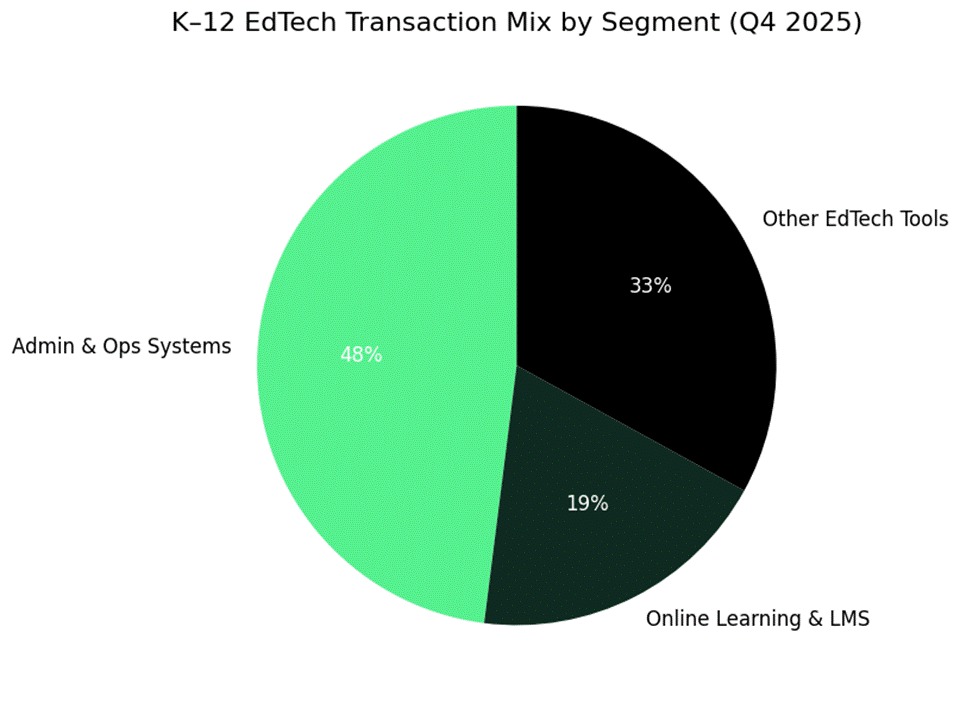

During Q4, administrative and school operations software captured the largest share of K–12 deal activity, followed by online learning and LMS tools. iv Superintendents and procurement officers prioritized vendors that could:

● Integrate with existing systems (SIS, finance) – new tools must plug into districts’ core student information and financial systems

● Offer predictable implementation – clear deployment timelines and minimal disruption

● Demonstrate impact on outcomes – evidence of boosts to compliance, attendance, or academic results

State budgets in late 2025 reinforced a mood of pragmatic optimism in K–12. Many states directed funds toward foundational needs and outcomes. For example, Colorado sustained its universal preschool and early intervention programs, Montana passed a $100 million act to raise teacher pay and expand career-technical education, and Texas pursued a dual strategy – increasing general K–12 funding by $8.5 billion while allocating $1 billion for education savings accounts targeting special-needs students (up to $30k per student). xiii Other states introduced outcome-based funding weights and teacher retention bonuses.

The common thread was investment in long-term quality over one-time experiments.

Deal activity in K–12 reflected this infrastructure-first orientation. For example, network and security provider Ednetics was acquired to strengthen school IT backbones, and NextGen Web Solutions expanded its footprint in enrollment and financial aid software – blurring the line between K–12 and higher-ed administrative systems. In the digital content arena, Newsela’s $100 million acquisition of Generation Genius broadened its curriculum offerings and underscored continued consolidation in K–12 content. iv

Public market performance echoed these priorities. Cash-flow-positive, renewal-driven operators led the pack. For instance, online school provider Stride, Inc. – trading at roughly 2.8× forward revenue and 11.6× EBITDA – outperformed many peers, highlighting investor preference for predictable, subscription-heavy business models.i Despite the progress in digital adoption, digital products still account for under 5% of total K–12 spending, leaving ample room for integration-driven growth in the coming years as schools modernize.

IV. Higher Education: Stability Before Strategy

Higher education entered late 2025 on firmer footing than it had seen in years. After two turbulent admission cycles, the 2026–27 FAFSA launched on time (with a soft open on October 1 and full deployment by December 1), marking a return to normal enrollment and financial-aid timelines.xi With these processes stabilized, institutions have been able to refocus on strategic improvements rather than firefighting.

Community colleges continued to be a bright spot – enrollments ticked up for the second consecutive term (over 3% year-over-year growth), driving renewed investment by institutions in student success infrastructure. Colleges are channeling resources into:

● Student success & advising platforms – to improve retention and graduation outcomes

● Credentialing and transcript tools – to streamline credit transfers and recognition of learning

● Integrated enrollment and financial aid systems – to unify recruitment, admissions, and aid workflows for efficiency

M&A activity in higher ed technology followed this workflow integration theme. Notably, digital content platform RedShelf was acquired by a strategic investor, and UK-based Enroly (which automates international student enrollment) was also picked up. iv These deals extend a broader consolidation wave aimed at building end-to-end student lifecycle suites – exemplified by moves like Ellucian acquiring EduNav (academic planning), Instructure buying Parchment (credentials), and Transact being rolled up under Roper Technologies (campus payments). The message: the market is rewarding solutions that tighten integrations and eliminate silos across the academic journey.

Institutions, facing budget pressures and accountability demands, increasingly favor platforms with clear ROI. Products that unify academic planning, student records, advising, and career placement – all while reducing administrative overhead – have the edge. Meanwhile, the pandemic-era vogue for fully outsourced Online Program Managers (OPMs) continues to fade. Universities are pivoting to more modular, in-house credential programs aligned with employer needs, rather than paying hefty revenue shares for external online program services.

Public company performance has been validating this focus on quality and usage. For example, language-learning leader Duolingo maintained a premium market multiple thanks to its high user engagement and recurring subscription revenue, reinforcing that investors reward sticky usage and strong unit economics.i

Overall, EdTech companies in higher ed are trading at higher revenue and EBITDA multiples than traditional education services firms, underscoring a market that values durable, usage-anchored models over flashy growth stories.

In short, the path forward in higher ed is less about splashy transformation and more about methodical modernization – slow and steady upgrades that improve institutional resilience and student outcomes.

V. Workforce Learning: The Sector’s Growth Anchor

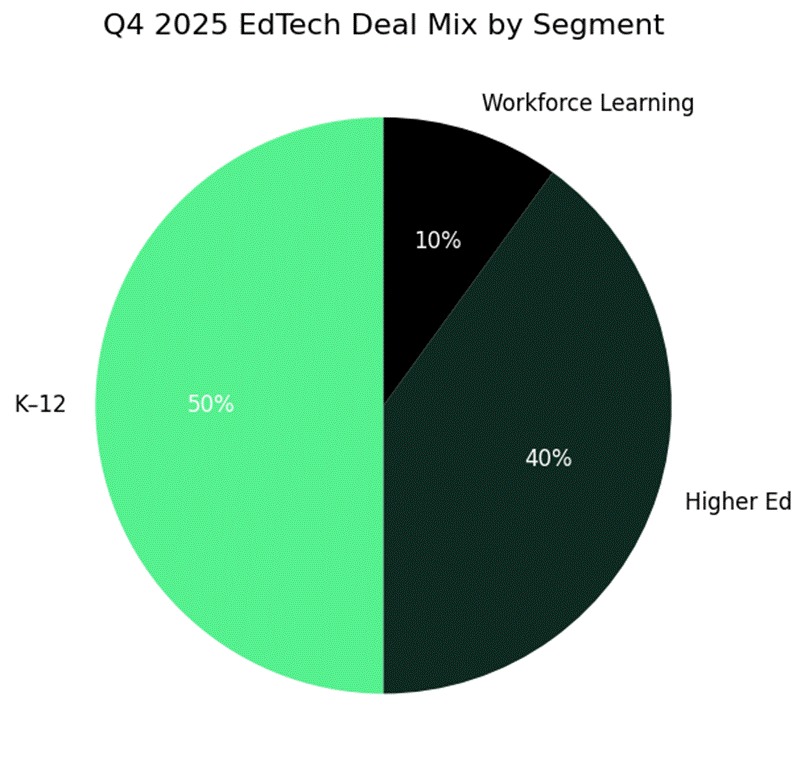

Workforce learning continued to be the growth engine of the EdTech market. In Q4 it represented only around 10% of deal count, yet it drew an outsized share of investor attention thanks to its tight linkage to employer needs and measurable ROI. Enterprises remain willing to spend on tools that directly upskill employees, ensure compliance, and boost productivity – a dynamic that keeps this segment buoyant even as others slow.

Public funding tailwinds also persist. The U.S. Department of Labor, for instance, has been investing heavily in apprenticeship programs (announcing $84 million in new grants during the summer), and the EU’s Pact for Skills reports millions of workers trained since 2020.v Both in the U.S. and Europe, these dollars flow into ecosystems that prioritize credentialed learning and job placement, strengthening the pipeline for workforce EdTech solutions.

On the corporate side, M&A targeted specialized capabilities to enrich larger platforms. For example, Ascendient Learning (focused on healthcare training) and Babington (business training) were acquired for their deep content in specific verticals. And in a move illustrating tech convergence, Cornerstone’s earlier acquisition of Talespin brought VR/AR-based soft skills simulations into a mainstream enterprise learning management system. iv Each of these acquisitions shows how platform players are bolting on features to offer more comprehensive, industry-specific learning solutions.

Public markets echoed these themes in Q4. Corporate e-learning leaders reported solid demand: Docebo cited strong enterprise uptake for compliance and frontline skills training, and Udemy Business continued to grow at a double-digit rate. The metrics that matter to investors remained consistent across workforce deals and companies, focusing on clear outcomes:

● Verified skill improvement – evidence that employees are gaining the competencies promised

● Higher retention & engagement – users returning regularly and completing training, indicating value

● Faster onboarding and upskilling – tools that quickly bring new hires up to speed or advance existing staff

Strategically, the verticalization of EdTech is accelerating in workforce development. Industry-specific learning stacks in areas like healthcare, automotive, and legal are emerging as critical infrastructure layers. These platforms integrate content, assessment, credentialing, and compliance tailored to a given sector, making them indispensable to employers in those fields. At the same time, AI is increasingly deployed to reduce content creation costs and improve assessment accuracy, which boosts margins and scalability for providers.

To investors, the workforce segment now looks like classic enterprise SaaS: sticky revenue, low churn, and plenty of expansion opportunity. Providers are boasting rising lifetime value-to-CAC ratios and have a clear runway for bolt-on acquisitions, making this arena a prime target for consolidation plays. In short, workforce learning has solidified its role as an anchor of growth and stability in EdTech portfolios.

VI. Investment Discipline: Metrics Over Momentum

Q4 2025 confirmed the new investor playbook in EdTech: the days of “growth at any cost” are over, and leaders win on metrics, not just marketing hype. Across K–12, higher ed, and workforce, top investors are concentrating their capital on companies that demonstrate:

● Retention – e.g. net revenue retention above 110%, indicating strong product stickiness and upsells

● Capital efficiency – implementation payback periods within ~12 months, showing quick ROI on deployments

● Tangible impact – clear, measurable improvements in student outcomes, operational efficiency, or employer ROI

The best-performing EdTech assets – both public and private – are those solving real pain points (compliance burdens, workflow inefficiencies, skills gaps) with verifiable results. In contrast, flashy front-end tools with only vague engagement stats are struggling to raise new funding or even to keep existing customers. Investors have become laser-focused on quality of revenue and evidence of impact.

Encouragingly, the macro outlook for EdTech is still positive even amid this more selective climate. Market projections remain supportive of long-term growth. HolonIQ estimates global digital education spend will reach $404 billion this year, roughly 5% of total education expenditures – leaving plenty of upside as digital penetration increases.ii In the U.S. alone, EdTech revenues are projected to grow from about $187 billion in 2025 to $348 billion by 2030, a healthy 13% CAGR.ii Within that expanding pie, new investment is clustering around “picks and shovels” infrastructure categories critical to the education system’s backbone, such as:

● Systems of record and enrollment engines (core databases and student onboarding systems)

● Payment and billing platforms (integrated tuition payment, financial aid disbursement, and billing tools)

● AI-powered productivity tools for teachers, administrators, and training managers (to automate tasks and personalize learning at scale)

● Vertical-specific credentialing and simulation platforms with strong compliance narratives (for fields like healthcare, finance, etc., where proof of skills and regulatory alignment are key)

Yes, capital is more selective than it was a few years ago – but it is far from absent. High-retention, outcome-verified companies can still command premium multiples in both M&A and late-stage funding.

In fact, the path to value creation in EdTech is clearer now than it has been in years: grow deliberately, integrate deeply into your users’ workflows, and prove your worth every step of the way.

VII. Outlook: Precision Over Pace

Looking ahead to 2026, EdTech is likely to behave more like a traditional enterprise software sector than a speculative high-growth story. We can expect slower headline expansion but higher-quality revenue, ongoing emphasis on profitability, and continued investment in core infrastructure themes. Key predictions by segment:

● K–12: Districts will keep consolidating point solutions into broader operational suites. Vendors that provide transparent usage analytics and tie product adoption to academic or budget outcomes will have an edge in increasingly competitive district RFP processes. The K–12 buyer is now focused on integration and accountability, so point tools will need to prove they can plug into the bigger picture or risk being phased out.

● Higher Education: With admissions and aid cycles normalized, colleges will make incremental but meaningful reinvestments in the student success stack – solutions for financial aid management, advising, degree planning, and outcomes tracking. We also anticipate continued growth in modular, employer-aligned credential programs, especially in disciplines with clear workforce demand (e.g. tech, healthcare, skilled trades). Rather than radical transformation, higher ed’s near future is about upgrading legacy systems and expanding career-connected offerings in a sustainable way.

● Workforce Learning: This trajectory remains the clearest. Employers will keep funding learning platforms that deliver verified skill gains, compliance assurance, and internal mobility. We should see further bolt-on acquisitions and vertical integrations in corporate learning, with platforms acting less as content libraries and more as talent infrastructure that ties learning directly to job performance and career paths. AI and data analytics will be key enablers here, customizing learning at scale and proving its ROI to enterprises.

On the investment front, deal activity may remain below the pandemic-era highs – likely under ~250 U.S. transactions per quarter on average – but the quality of capital will continue to rise. Minority growth rounds, structured investments, and targeted platform acquisitions are expected to dominate the deal landscape through 2026. In this environment, companies that clear the high bar on retention, impact, and payback will find robust and competitive investor demand when they do seek capital.

Overall, digital penetration in education is still low, but conviction in its value is growing steadily. As leaders at school districts, colleges, and corporations increasingly prioritize durable value over shiny novelties, EdTech is entering its most stable and strategic phase to date. It’s no longer viewed as a speculative bet on the future – it has become critical infrastructure for how learning happens today.

References

[i] Finro Financial Consulting. (2025, November 16). EdTech Valuation Multiples: Q4 2025 update. Finro Financial Consulting. https://www.finrofca.com/news/edtech-multiples-q4-2025

[ii] HolonIQ. (2025a, December 16). Education in 2030: Five Scenarios for the Future of Learning and Talent [Report]. HolonIQ. https://www.holoniq.com/2030

[iii] HolonIQ. (2025b, December 16). 2025 Global EdTech 1000 – Benchmarking the most promising EdTech startups from 2025. HolonIQ. https://www.holoniq.com/notes/2025-global-edtech-1000

[iv] PitchBook Data, Inc. (2025, October 28). Seed Under Pressure: High seed prices and extended private lifecycles pressure seed returns [Analyst Note]. PitchBook Data, Inc.

[v] Whiteboard Advisors. (2025, December 18). Workforce Pell Rules Take Shape; States to Play a Major Role in Implementation. Whiteboard Advisors. https://whiteboardadvisors.com/workforce-pell-rules-take-shape-states-to-play-a-major-role-in-implementation/

[vi] Whiteboard Advisors. (2026a, January 9). Can Edtech Still Make the Case for Itself in 2026? Whiteboard Advisors. https://whiteboardadvisors.com/can-edtech-still-make-the-case-for-itself-in-2026/

[vii] Whiteboard Advisors. (2026b, January 16). Plugged Out: What the Senate’s Youth Technology Hearing Signals for Education, Edtech, and AI Policy. Whiteboard Advisors. https://whiteboardadvisors.com/plugged-out-what-the-senate’s-youth-technology-hearing-signals-for-education-edtech-and-ai-policy/

[viii] Whiteboard Advisors. (2026c, January 10). State of the States: Our Analysis of Governors’ Speeches, YTD 2026. Whiteboard Advisors. https://whiteboardadvisors.com/state-of-the-states-our-analysis-of-governors-speeches-ytd-2026/

.jpg)