Making Sense of Equity Accounting for Growth-Stage Companies

As businesses expand, invest in other businesses, and build partnerships, their financial reporting needs become more complex.

As businesses expand, invest in other businesses, and build partnerships, their financial reporting needs become more complex. One area that needs attention is equity accounting — which comes into play when a company holds significant influence, but not complete control, over another entity. Growth-stage companies, private equity firms, and venture investors can use equity accounting to accurately reflect the value of minority stakes.

What is Equity Accounting and When is It Used?

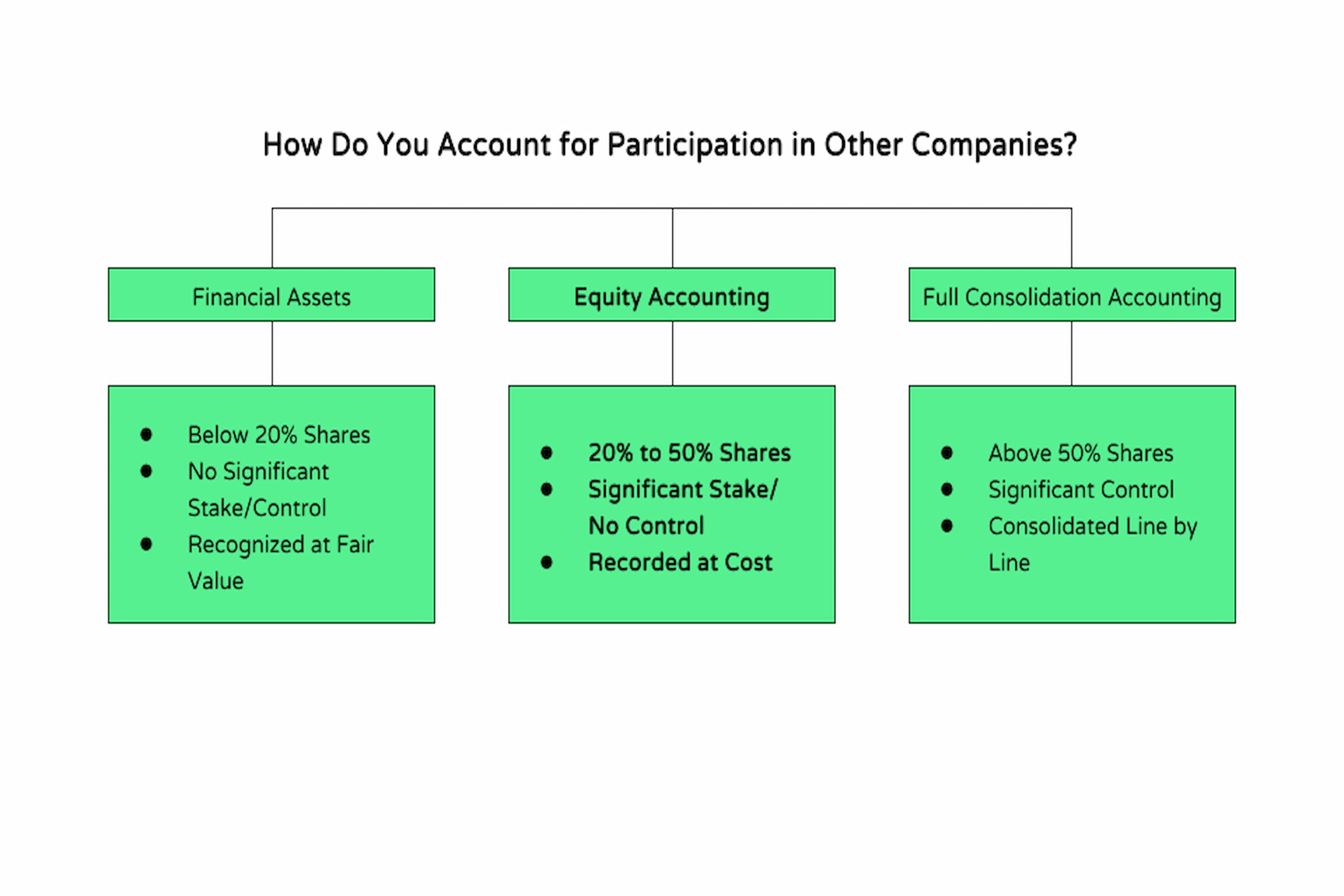

Equity accounting, or the equity method of accounting, applies when an investor has significant influence over another company (called an "associate") but does not control it. This usually happens when the investor owns around 20% or more of the voting stock. Instead of consolidating the financials of the two separate companies, the investor reports its share of the associate’s profit or loss and adjusts the investment value on its balance sheet.

This approach gives a more realistic picture of the investor’s ongoing relationship with the associate.

For example, if a company buys a 25% stake in another firm, and that firm earns $200,000 in profit, the investor adds $50,000 to the investment’s carrying value to reflect its 25% share of profit.

Why Is Equity Accounting Important for Growth-Stage Companies?

Growth-stage companies often bring in minority investors, engage in joint ventures, or invest in complementary businesses and startups. These relationships fall under the scope of equity accounting.

Some common examples include:

- Venture or private equity firms tracking the performance of smaller investments

- Companies partnering with suppliers or tech firms through equity stakes

- Corporations investing in startups that support their bigger goals

In these situations, equity accounting provides a transparent, performance-based view of how these investments are performing — helping leaders manage their money, create accurate reports, and build trust with investors.

How Does Equity Accounting Work?

The equity method includes updates that show changes in the associate company’s financial performance:

1. Initial Recognition

The investment is recorded at cost when acquired, including transaction costs.

2. Share of Profit or Loss

Each period, the investor records its proportionate share of the associate’s income or loss, based on their ownership.

3. Dividends

Dividends received are treated as a return of capital rather than as income, and they reduce the carrying value of the investment.

4. Impairment

If the investment loses value due to operational issues or market conditions, it must be impaired—meaning its value is reduced in a company’s books.

For example, if a company buys a 30% stake in another business for $1,000,000. If that business posts a $50,000 net loss, the investor reduces the investment’s value by $15,000, bringing it to $985,000.

What Are Some Common Challenges of Equity Accounting?

While the equity method is straightforward, there are some obstacles a growth-stage company might face:

- Limited financial infrastructure: Many growing companies lack the tools to track changes regularly.

- Access to information: The associate company might complicate reporting by not providing timely or detailed financials.

- Impairment judgments: It’s not always clear when a decline in value is permanent.

How Would A Company Know if Equity Accounting Applies?

Here are some questions companies should consider when deciding if equity accounting applies to them:

- Do we own between 20% and 50% of another company?

- Do we have influence over key decisions, such as a board seat or veto rights?

- Do we have access to the associate’s financials and are they reliable?

- Have any dividends been declared or paid?

- Are there warning signs such as consistent losses or legal risk?

Answering “yes” to the first two questions typically signals that equity accounting is required. The other questions help make sure the equity accounting is being handled right.

How Does Equity Accounting Support Smart Decision-Making?

Equity accounting offers insight into the health of a company’s investments. For leadership, this helps answer questions like:

- Are our investments adding value?

- Are we allocating resources in the best ways?

- Are there any investments that need a second look?

By tracking the performance of minority investments over time, companies can improve planning, evaluate partnerships, and offer more visibility and confidence to investors or acquirers.

Final Thoughts

As companies keep growing through partnership and minority investment, equity accounting has become more integral and important. It ensures that companies reflect the true economic performance of their investments — not just the upfront cost. This clarity can provide valuable insights.

For growth-stage businesses, the equity method supports better decision-making, sharper capital management, and better communication with investors. And it isn’t just an accounting necessity — it’s a strategic advantage.

If you have questions about equity accounting, please reach out.

.png)